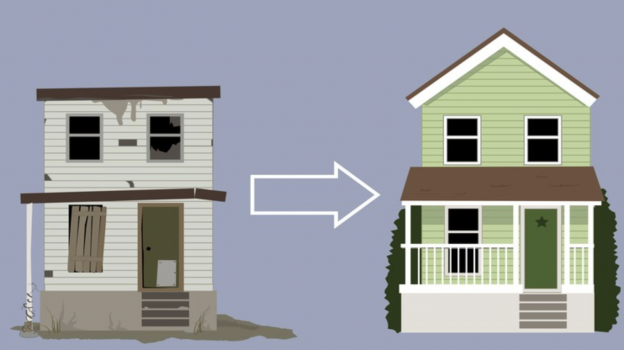

A fix and flip real estate is well known successful business with profit or ample of gain on every property. Perhaps, the business looks so simple and easy, but it is not as what it looks. Many television shows are forecasting live and recorded programs filming that the fixing and flipping process of a property is quite easy and all it requires is nothing but owning a property and undertaking few cosmetic fixes and therein subject to re-sale for considerable profit. The entire thesis is not exactly true unless the television show replicate the possibilities of loss accompanying the fix and flip real estate if not cautious steps are followed while reselling process.

It is better to have a broader view all about the fix and flip real estate business inclusive of the danger zones that cover up. Expert’s advice seems to be fruitful for in the case of novices to avoid the unnecessary expenses while fixing the property. They advice to buy a property after getting known about future to fix and flip and worth of the property to undertake the minor to major fixing processes. Beginners are instructed to own small scale property instead buying mega budget houses or building. It is taught to them to avoid large and huge loss when actual profit is not liable to gain.

Additionally, beginners are asked to cross check and go through all the legal clearance of the property before go for cart. The legal clearance is must to avoid unnecessary chaos that arise after repairing the property either house or some other building and exposed to flip the same. Above all, the investors are asked to know the after repair value of the house or building and calculate whether the property brings actual profit after flipping. Basically, what does the after repair value mean exactly? How can an investor calculate the same for knowing the profit?

Here comes the answer for above questions from the experts who explains their followers regarding calculating the profit and loss proportion in every property after fix and flipping. Simple terms of after repair value indicates that the actual profit that is gained on flipping a fix property that has bought at considerable low cost. 70% rule indicates how to calculate an after repair value of a property?

After repair value = purchase price of building + cost of renovations.

Exactly, the value of building after renovated will be rising tremendously to certain hike in proportion from which the cost of renovation is deducted which will give the result to the after repair value of the building, in other words, the profit gained in the fix and flipping of a house.

But it is up to the investors section or portion to decide what is there to fix or to make renovations in particular property. Investors are insisted not to undergo unwanted recreations unless if there is necessary and rational rise of the property value. Mere large budget cosmetic renovation does not bring any kind of profit that is expected to own. Hence, it is the proclaimed rule or suggestion from the expert point of view to avoid mere wages to expense. Similarly, they also insist not to invest in huge valued property that is not to invest huge money for buying a property or building for fix and flipping. This is done so as to avoid unexpected loss if not the building or the house sold out on expected estimation. Cautions are applicable before buying any property and underplay the fixing processes without scope for re-gaining from the property.

Safer side to invest in buying a house or any sort of building is to achieve the HELOC abbreviated as Home Equity Line Of Credit or the mortgage loan that helps to buy a property to undertake fix and flipping for more profit. The concept will help the investors to buy the house or building using a Miami property search finds. The loan service desperately will enable to deduct the percentage of interest that is achieved in the process of loaning but not will deduct the returns of the

A Miami Public Adjuster, hopefully, will help the investors, buyers and the vendors in turn to find out maximum returns in the name of gain. Above all, it is necessary to know the value of vendors who sell the property for fix and flipping. The authenticity of the vendor along with the property is gaining equal importance before stepping into the process of fixing and flipping. Legal documents of the vendors are also a very important factor to cross-check and considering all the amenities of the property whether the property is free from all the damages.

Every State, County and the City or

It is up to the interest of the investor who suggests fixing the damaging system on the short scale or in the large scale. Public adjuster proclaimed to assist all the investor, vendor and the buyer in the case of